- by Yueqing

- 07 30, 2024

-

-

-

Loading

Loading

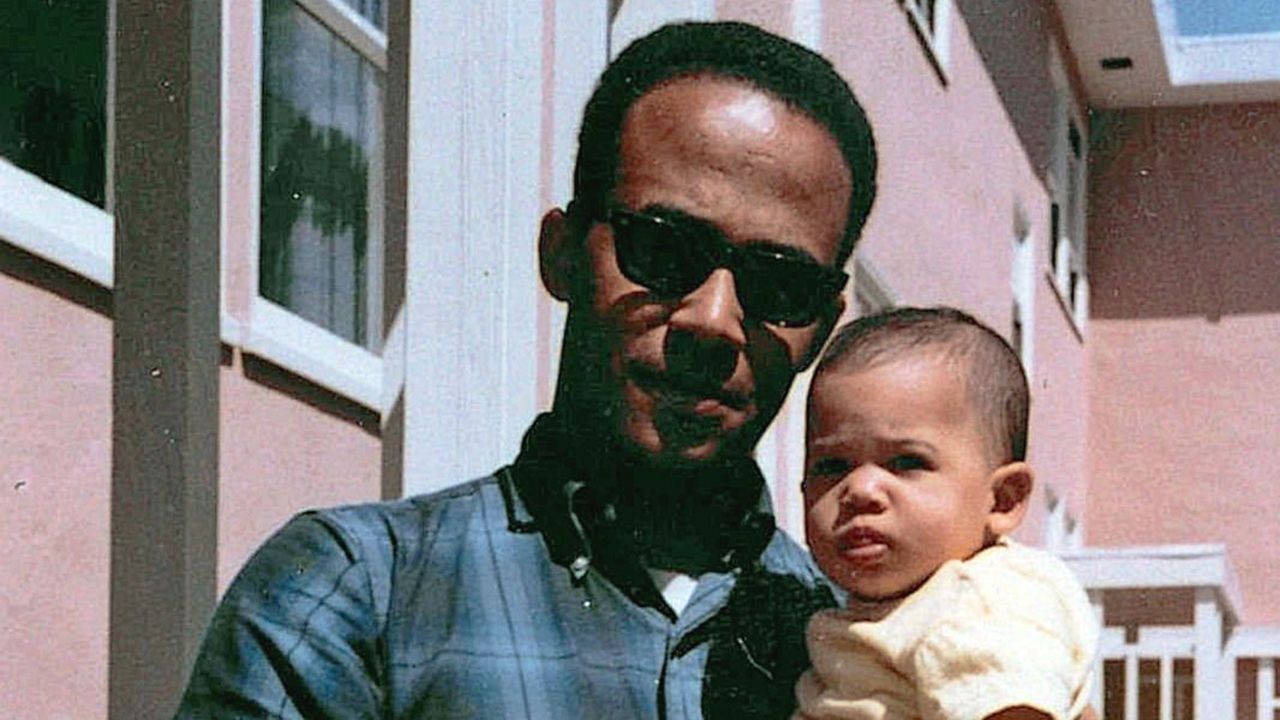

SEVEN OR EIGHTGDP times a day, aggrieved creditors would call Liang Wenjin demanding payment. A resident of Shenzhen, an entrepreneurial Chinese city bordering Hong Kong, Mr Liang had started a business in 2018 making Bluetooth headsets. But his company failed to connect with the market, and covid-19 dealt a final blow. Mr Liang returned to work as an engineer. But his debt of 750,000 yuan ($115,000) remained, a lingering weight on his finances and his mind.Debts like Mr Liang’s have risen quickly. From less than 40% of in 2015, household loans exceeded 62% at the end of last year. The biggest chunk was mortgage debt, a by-product of China’s runaway property market. “Operating loans” of the kind weighing on Mr Liang accounted for about a fifth of the total.